How to Avoid Trigger Leads and Keep Your Credit Safe When Shopping for a Mortgage

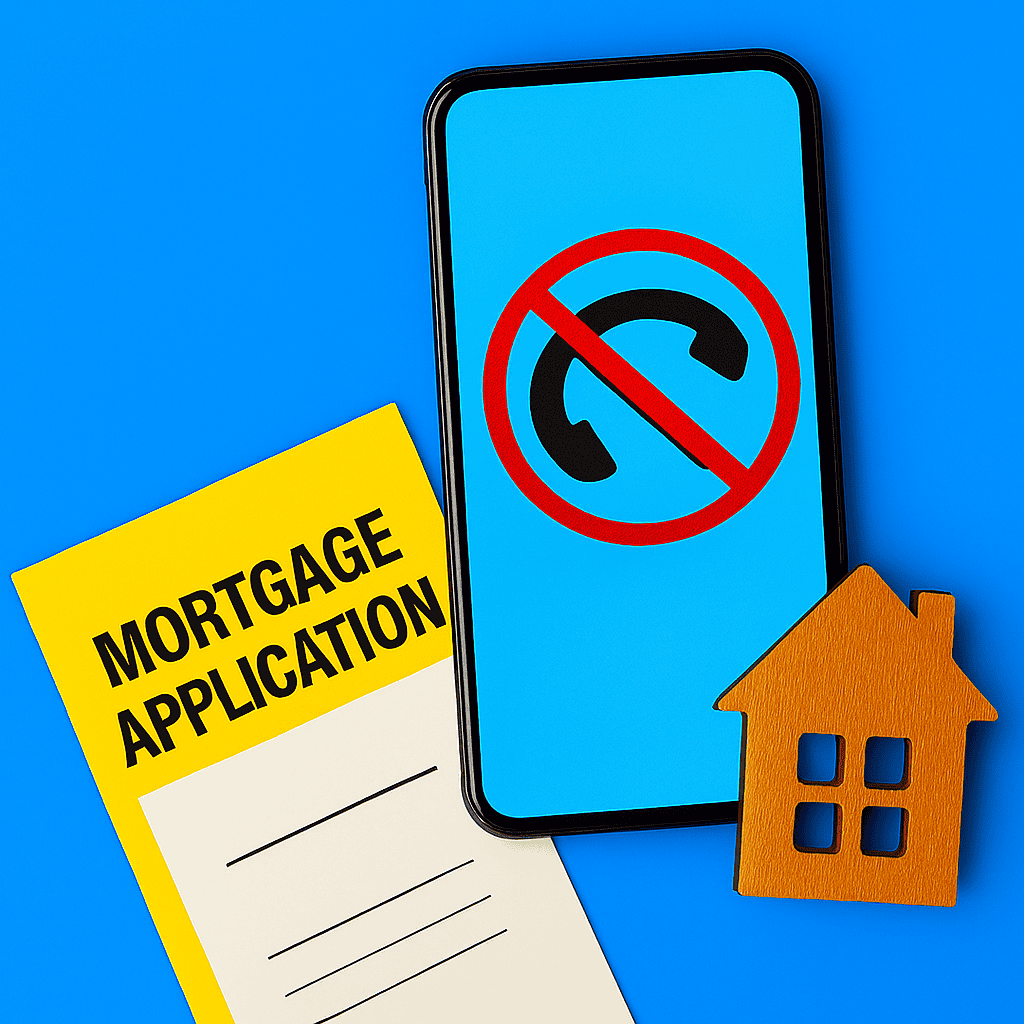

If you're about to apply for a mortgage, there's a hidden risk you probably haven't heard about, but it affects nearly every buyer: trigger leads.

When a lender pulls your credit report, the credit bureaus (Equifax, Experian, TransUnion, and Innovis) can legally sell your information to dozens of other lenders and marketing companies. These are called “trigger leads,” and they instantly alert competitors that you’re shopping for a mortgage.

The result? Your phone and inbox start blowing up with spam calls, texts, and offers you never asked for.

That’s not just annoying—it’s dangerous for your credit, your privacy, and your ability to focus on the real task: buying a home.

Here’s how to stop it before it starts:

Step 1: Opt Out at OptOutPrescreen.com

Visit www.optoutprescreen.com and select the permanent opt-out option.

This removes your name from lists used by credit bureaus to market pre-approved credit offers. It’s one of the most effective ways to avoid trigger leads altogether.

Step 2: Use a Soft Pull for Pre-Qualification

Ask lenders if they can offer a soft credit pull to provide your pre-approval or rate quotes.

A soft inquiry doesn’t create a trigger lead, and it won’t affect your credit score. Many reputable lenders now offer this option up front.

Step 3: Be Strategic, Don’t Apply Everywhere

Some buyers believe applying to five or more lenders improves their chances or gets them better rates. The reality?

-

Multiple applications mean multiple hard inquiries. That can lower your credit score.

-

Each pull increases the likelihood that your information will be resold or mishandled.

-

If applications aren’t submitted within a tight window (14 days for most FICO models), your credit takes the full impact.

Instead, choose one well-vetted lender, or work with a broker or marketplace that can shop multiple programs off a single credit pull.

Step 4: Exercise Your Legal Right to Opt Out of Data Sharing

Under the Gramm-Leach-bliley Act (GLBA), lenders must give you a privacy notice and a way to opt out of sharing your information with third-party companies.

After you apply, take this extra step:

-

Read the privacy notice carefully

-

Send a written email or letter that says:

“I invoke my GLBA opt-out rights. Do not share my non-public personal information with non-affiliates except as required to process my loan.”

Save a copy for your records.

Step 5: Temporarily Freeze Your Credit if Needed

For added security, consider placing a temporary credit freeze with all three major bureaus. It adds a layer of protection from unwanted offers and potential identity theft. You can lift the freeze when you’re ready to move forward with your chosen lender.

Final Thoughts

Buying a home is one of the biggest decisions of your life, and you shouldn’t have to deal with unnecessary spam, privacy risks, or credit hits just to get a mortgage quote.

The smart, strategic move is to protect your data before the first lender pulls your credit. Then work with professionals who respect your privacy and your time.

If you need help finding a trusted lender who follows these best practices, I’m here to guide you.

Connect